On June 12, 2026, tech stock analyst Beth Kindig published a deep-dive report on IO Fund with a provocative title pointing directly at a sensitive topic: the “circular financing” between Nvidia, CoreWeave, and Nebius. The article scored 126 points and 43 comments on Hacker News — in the tech community, this topic hits a nerve.

The takeaway is almost absurdly simple: the company that sells GPUs lends you money so you can buy its GPUs. You take the money, buy the GPUs, and the cash flows right back to them. Oh, and now you’re deep in debt.

Who Are These Companies?

First, the cast.

Nvidia — the undisputed king of AI GPUs. Over 90% of the chips training large models today are Nvidia’s. In 2026, its free cash flow is $119 billion — second globally only to Apple.

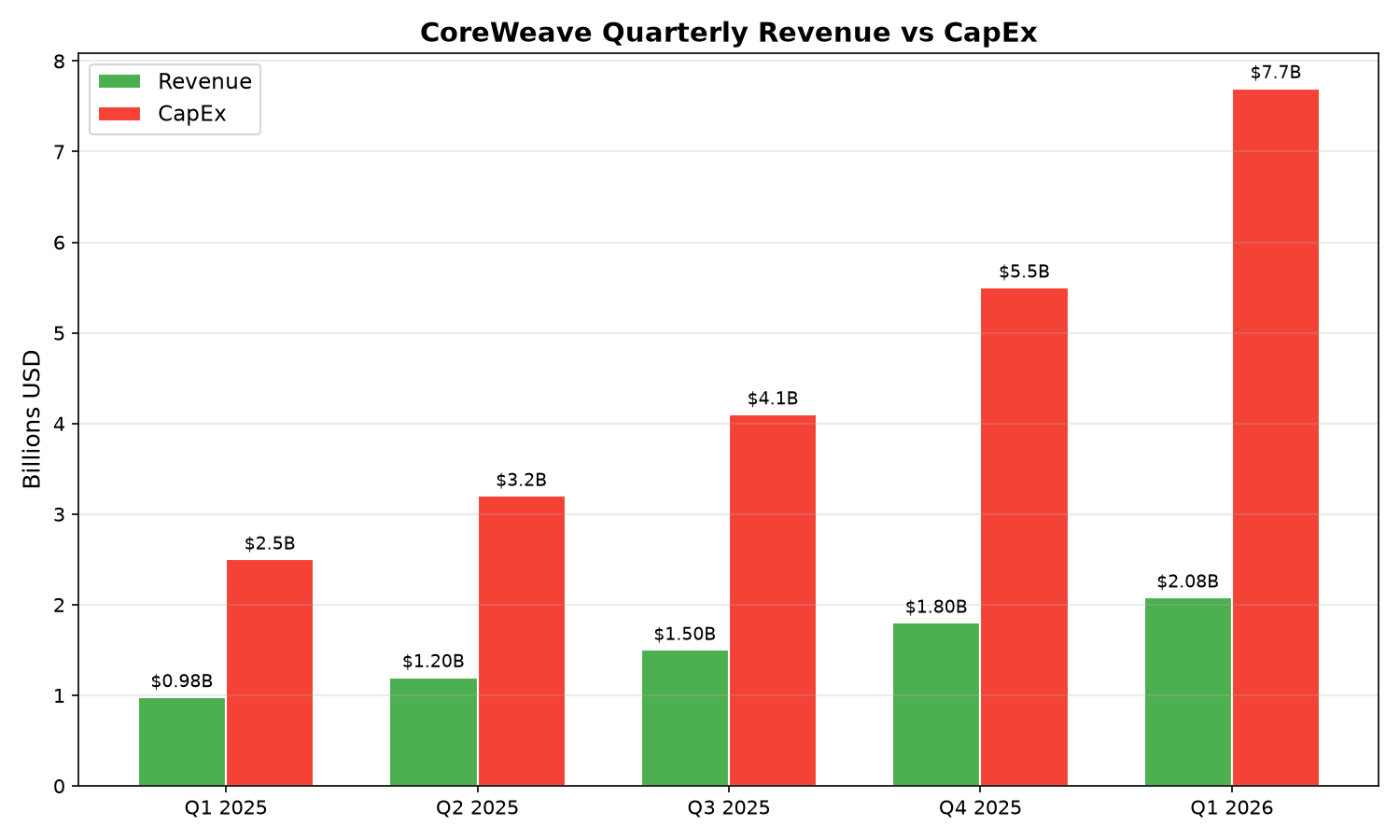

CoreWeave — a “neocloud.” It doesn’t develop AI models. It does one thing: buys Nvidia GPUs, builds data centers, and rents compute to companies that actually need to train AI — Microsoft, Meta, OpenAI. Q1 2026 revenue: $2.08 billion. Capital expenditure: $7.7 billion. Earns $2, spends $7.70.

Nebius — another neocloud, European roots. Same model: buy GPUs, build data centers, rent compute. Q1 revenue: $339 million, up 684%, sounds impressive. CapEx: $2.47 billion. Still spending more than it earns.

How the Money Circles

The circular financing structure can be explained with a familiar analogy.

Imagine you’re a car manufacturer who wants more people to buy your cars. But customers don’t have the cash. So you invest in your customers’ companies. They take your investment, add some bank loans, and buy your cars. Your sales look great. Your customers get cars to run taxi businesses.

Whether this model works depends on one question: Can the taxi business earn enough to pay off the car loans?

In AI, the loop looks like this:

Step 1: Nvidia invests. In 2026, Nvidia invested $2 billion each in CoreWeave and Nebius. This isn’t Nvidia’s first time — it already held roughly $900 million in CoreWeave shares.

Step 2: Neoclouds leverage up. CoreWeave and Nebius take Nvidia’s investment and go issue debt. CoreWeave’s total debt: $24.86 billion. Nebius: $8.45 billion. And the collateral for these loans? — the very GPUs they bought from Nvidia.

Step 3: Buy GPUs, money flows back to Nvidia. With investment cash and loans in hand, both companies go on a GPU buying spree. CoreWeave plans $33 billion in capEx this year (mostly GPUs), Nebius plans $22.5 billion. The $2 billion Nvidia invested unlocks hundreds of billions in purchase orders — and the GPU sale revenue flows right back to Nvidia.

Step 4: Rent compute, service the debt. CoreWeave and Nebius deploy those GPUs in data centers and rent compute to Microsoft, Meta, OpenAI, and others. These big customers have signed long-term contracts — Microsoft and Meta alone have committed $122 billion. The neoclouds are betting rental income will cover the debt and interest.

A Perfect Loop, or a Dangerous Cycle?

You might be asking: what’s wrong with this? Isn’t this just normal business investment?

The problem is in the numbers.

Number one: crushing interest payments. CoreWeave’s Q1 interest expense: $536 million — 25.8% of revenue, 46.3% of adjusted profit. For every $100 you earn, $26 goes to interest. By Q2, this is projected to hit 27.3%. And this is against a rising rate environment — 3-year Treasury yields went from under 3.6% at the start of the year to nearly 4.2%, pushing CoreWeave’s borrowing costs higher.

Number two: cash burning fast. CoreWeave’s Q1 free cash flow: negative $4.71 billion. Cash reserves dropped $890 million in a single quarter to $2.27 billion. At this rate, without new financing, cash won’t last. And it still has $25.3 billion in capEx commitments this year.

Number three: contracts dwarf revenue by an order of magnitude. CoreWeave expects $12.6 billion in revenue this year, Nebius $3.4 billion. But Microsoft and Meta alone have committed $122 billion in future orders — nearly 8x these two companies’ combined annual revenue. Big promises, but deliverability depends on whether the big customers’ AI demand holds up.

Nvidia Isn’t Doing Charity

One detail deserves special attention: Nvidia isn’t just an investor — it’s also a backstop.

According to CoreWeave’s disclosures, Nvidia signed a $6.3 billion agreement — if CoreWeave’s GPU compute goes unrented, Nvidia commits to buying the remaining unused compute itself, effective through April 2032.

What does this mean? It’s like lending a friend money to open a restaurant and also signing a deal that if the restaurant is empty, you promise to eat there every day and pay out of your own pocket. The friend’s risk is dramatically reduced — but what about yours?

Nvidia’s logic isn’t hard to follow. It needs a compute channel it controls, independent of the big cloud providers (AWS, Azure, Google Cloud). Those hyperscalers are developing their own AI chips and may reduce their reliance on Nvidia over time. Propping up independent neoclouds like CoreWeave and Nebius creates a set of “loyal customers” — they buy only Nvidia GPUs, use Nvidia’s full technology stack, and feed usage data back to Nvidia for next-gen chip improvements.

Spending $2 billion to unlock hundreds of billions in purchase orders while hedging against big customers defecting — that math works for Nvidia.

The Villain: When Financial Engineering Replaces Real Demand

Let me be clear. Circular financing isn’t inherently a problem. Many industries have supplier-invests-in-customer arrangements. But AI’s version has two features that make it dangerous.

First, the leverage is extreme. CoreWeave and Nebius are, at bottom, betting the farm. They’re betting that AI compute demand will keep exploding, that enough GPUs will rent at high enough rates to pay off the debt. But their debt is growing far faster than revenue. Since its IPO, CoreWeave has issued $18.81 billion in debt versus $3.5 billion in equity — a 5:1 debt-to-equity ratio.

Second, cracks in the demand story. Why do Microsoft and Meta rent from neoclouds instead of building their own data centers? Partly because neoclouds can deploy GPUs faster (weeks versus years for in-house builds). But Beth Kindig points to a subtler motive: converting capital expenditure into operating expenditure.

What does that mean? When Microsoft builds its own data center, the money hits the balance sheet all at once, hitting free cash flow. Microsoft’s 2026 capEx is projected at $190 billion, with cash inflow of $200 billion — that’s 95% of cash consumed by capEx. But if it signs lease contracts with CoreWeave, costs are amortized over years, don’t count as capEx, and the financial statements look prettier.

In other words, neoclouds exist partly because big tech is doing accounting magic. If AI demand cools, or regulators change the accounting rules, those billion-dollar lease agreements could turn into worthless paper overnight.

Bubble or Real Value?

One top-voted HN comment gets to the heart of it:

“It’s not the money itself, it’s the model. You invest in a startup, sign long-term contracts; that startup uses your money plus mountains of debt to build data centers and buy GPUs; your financials look great. The question is: what happens when they run out of money and can’t borrow any more?”

The answer depends on whether you believe AI compute demand will keep growing forever.

True believers point to ChatGPT’s 200 million weekly active users — every query burns GPU compute. Future software will embed AI everywhere, inference demand only grows. CoreWeave and Nebius hold billion-dollar contracts with top-tier clients. As long as demand holds, rent flows, debt gets paid.

Skeptics counter: what if AI model efficiency keeps improving (same task, less compute)? What if big customers start building their own data centers? What if next-gen chips depreciate old ones faster — GPUs have roughly a 6-year depreciation cycle, but Nvidia’s release cadence is accelerating? You took out loans for H100s and before they’re paid off, the B200 arrives at double the performance and similar price. What’s the collateral worth then?

D.A. Davidson analyst Gil Luria’s assessment of CoreWeave is blunt: “This is a company that destroys value rather than creating it.”

I’m not qualified to judge who’s right. But one thing is clear: when an industry’s growth depends increasingly on financial leverage — borrowing to buy growth — rather than real operating profits, it’s playing a dangerous game. The game can keep going — until the day nobody is willing to lend anymore.

References: